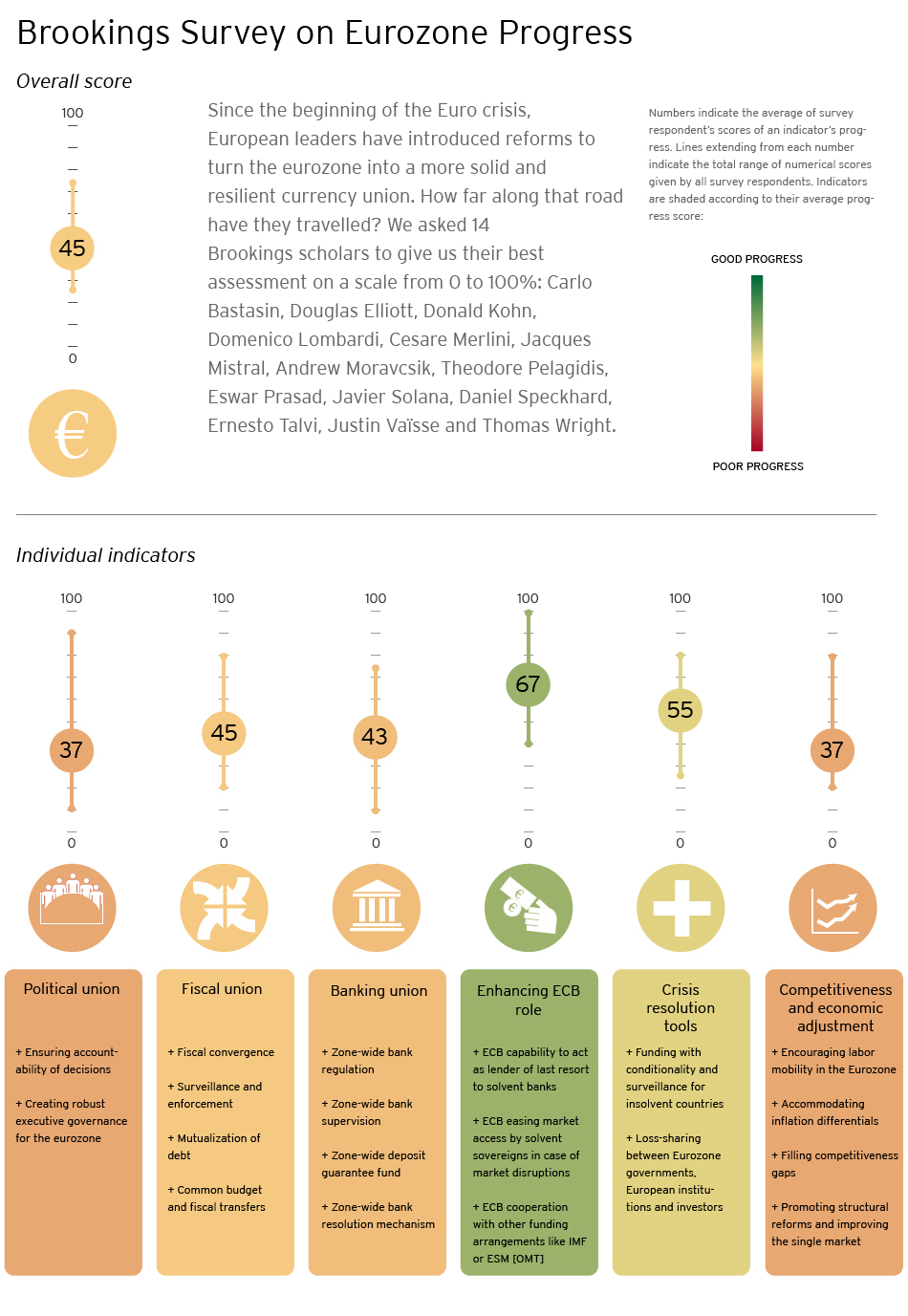

"On a scale from 0 to 100%, how far along do you estimate the eurozone to be in reforming itself in order to be a viable currency union in the long term?"

Eswar Prasad

Senior Fellow, Global Economy and Developmen; New Century Chair in International Trade and Economics

25

"Far too many divergent interests in both short and long term.

"

Andrew Moravcsik

Nonresident Senior Fellow, Foreign Policy, Center on the United States and Europe

30

"In the end, the Euro stands or falls on structural reform and the Europeans are only 20% there, if that. Everything else is managing liquidity problems without dealing with underlying solvency issues. The best one can hope for from that is continuation of the unsatisfactory status quo. If survival of the Euro is the goal, I am modestly "optimistic" in the short-term and pessimistic in the long-term. If growth is the goal, I am pessimistic in the short-term and neutral in the longer-term."

33

"The eurozone has made significant progress in outlining a number of steps toward greater economic union as a necessary accompaniment to currency union. But in many respects, these steps—e.g. greater fiscal and banking union, support for the bond markets of trouble peripheral states engaged in reform—have yet to be implemented, in part because they are meeting resistance from countries both in the center and the periphery. Moreover, the sustainability, both politically and economically, of fiscal correction and the internal devaluation process to restore competitiveness in the periphery through austerity and recession is an open question as is the willingness of the center to provide support to the periphery to ameliorate the pain. Finally, the needed surrender of sovereignty of the individual countries to the collective will needs to be supported by governance reforms to enhance the democratic accountability of the collective and enable it to make decisions more readily."

35

"Important progress has been made in terms of announcing important policy innovations and a consensus on the way forward has finally emerged. However, credible implementation is key and, on that, there is still a very long way ahead of us.

"

Thomas Wright

Fellow, Foreign Policy, Managing Global Order

35

"Europe has embarked upon the path but there is a long way to travel. It gets to 35% for wanting to succeed and taking important initial steps but to progress further the eurozone will need to show itself capable of changes that are very difficult politically.

"

Carlo Bastasin

Visiting Fellow, Global Economy and Development, Center on the United States and Europe

40

"Overall the institutional setting is very wanting. The lack of decisive countermeasures to the crisis is evident both in terms of financial resources aimed at staving off a short term emergency, and in terms of medium-long term institutional framework for more convergence and integration in the euro area. In fact the October EU Council has scaled down the objectives of the reforms for a more genuine economic and monetary union, while there is little doubt that the crisis is far from over. The strategy of stabilizing the fiscal position of the States while the private sector's deleveraging is still underway has backfired. The debt deflation spiral has now an own inertia that is becoming more difficult to reverse without economic coordination. The deterioration of the economy is having effect on political consensus for Europe, but the eurozone political response remains based on homogeneous binding and obligatory rules that leave no scope for real management of a non-homogeneous area. However, four times the final blow to the euro has already been averted in the last four years. So we should assume that, in case of a recrudescence, the political will to save the euro will be found and the ECB will step in again.

"

Douglas Elliott

Fellow, Economic Studies, Initiative on Business and Public Policy

40

"Many of the basics exist for a stable eurozone, which has allowed the currency zone to avoid collapse so far despite the severe crisis. Much more would need to be done to ensure stability. Some of this has been promised, but not yet delivered, while other pieces are not even agreed upon in principle.

"

Justin Vaisse

Director of Research, Center on the United States and Europe; Senior Fellow, Foreign Policy

40

"Markets and foreign governments now seem to believe that the Euro is here to stay and will reform itself. They are right, even though the eurozone has not yet reached a sufficient level of progress to be confident that it would survive renewed internal and external tensions, crises and shocks. Moreover, the appetite for reforms fades away as soon as confidence is restored, which puts the whole process into question. In this regard, the banking union will be a major test for European leaders. And while the ECB role is the uncontested bright spot of the process, the current deflationary debt spiral could imperil all these institutional efforts.

"

Cesare Merlini

Nonresident Senior Fellow, Foreign Policy, Center on the United States and Europe

51

"The average of my assessments above is 51, that is just a bit inside the 50 to 75% bracket. With the meaning given to such bracket (confidence in the long term, but with risks), that broadly corresponds to my evaluation: we may be halfway through the reform process of the eurozone."

Daniel Speckhard

Nonresident Senior Fellow, Foreign Policy, Center on the United States and Europe

60

"I believe a eurozone will survive these current challenges, but it is still not clear whether it will survive in its present form. While this overall estimate is higher than probably one would arrive at from my sub-estimates, this is primarily due to the EU continually surprising me over the longer term with its ability to lurch forward when things look the most difficult and when the political costs of inaction are higher than the costs of increasing transfers or giving up more national sovereignty.

"

75

"The EMU is not an optimal currency area, this is not surprising, as you don't reveal pre-existing 'optimal currency areas' through a sudden and definitive political decision; optimal currency areas are the result of an endogenous process, this is at least what American history suggests and also one of the two competing academic positions in the debate of the 90's. So far, the EMU is an empirical confirmation of this proposition by proving its ability to resist the most severe and repeated financial shocks. Through continuous negotiations and rescue operations, members countries have confirmed the choice of the EMU: It took only two years for 17 governments to come to a shared understanding of the causes of the sovereign debt crisis and to a vision of the complex and multi-dimensional solution. The willingness to build a 'more perfect monetary union' has been sealed by the governments in their June 2012 summit with the adoption of the '4-President' Report; the ECB has offered ample time and ammunition to make this complex political process come to fruition. The process is moving forward; it can still face brutal shocks and will in any case rely on difficult and sometimes tense negotiations but the main dangers now could come from a depressed economic outlook making every choice more difficult or from complacency in a less pressing financial environment."

"In order to make the eurozone a viable currency union in the long term, European leaders need to make progress towards political union, both to strengthen its governance and remedy its executive deficit, and to ensure democratic accountability. On a scale from 0 to 100%, how far along do you estimate the eurozone to be in achieving the necessary level of political union to be consistent with a very resilient eurozone?"

Domenico Lombardi

Senior Fellow, Global Economy and Development

10

"This is by far the area where the least progress has been made. Clearly, the crisis has highlighted the unsustainability between a highly-integrated monetary, financial, and economic area and its lack of a political union. This tension has now been acknowledged but little or nothing has been done."

Carlo Bastasin

Visiting Fellow, Global Economy and Development, Center on the United States and Europe

20

"Political integration is still determined by the will of national governments. Their resolve to delegate sovereignty is still to be tested. Until now national monopoly over the crisis has been the major cause of delay in the solution of the euro crisis. Each time that the crisis eases, national governments abstain from moving toward more integration. The political footprint remains the rule-based one adopted with the Maastricht Treaty at the light of expected convergence of the economies. It is hardly workable in the context of increasing divergences. Furthermore the blueprints for political union under discussion – as well as the Treaty (TFEU) - give only a very limited authority to the European Parliament that has until now not been able or willing to use its powers in order to change recommendations for euro area countries."

20

"Although a parliament is in place, most important decisions seem to be made among the leaders of a few countries and need to be adopted by all 17, only indirectly imperfectly and representing the views of the majority of the people of the eurozone. The executive in particular needs a better system of democratic accountability."

20

"The eurozone has decided that it wants to survive and will make a great effort to construct a viable union. This is very significant. But, it is not sufficient. State building is extremely difficult and we are very early in the process. Many roadblocks exist—technical, political, and external—which could derail the project, especially if a new crisis or accident occurs before it is completed."

Douglas Elliott

Fellow, Economic Studies, Initiative on Business and Public Policy

30

"On the positive side, the structure of the EU, complemented by the ECB for the eurozone, provides the core for true political union. It has executive, legislative, and judicial arms with some considerable history and relatively smooth operations. On the negative side, national governments have deliberately kept the power of the European institutions fairly limited. Further, the Euro Crisis has shown that those European institutions can accomplish little at this point in their development without strong support by key national governments."

Cesare Merlini

Nonresident Senior Fellow, Foreign Policy, Center on the United States and Europe

30

"I have problems with political union as a prerequisite of currency union. The yielding of fiscal sovereignty – a political act – is already taking place as far as the countries at risk are concerned. But a political union has implications that are permanent and extended to all eurozone countries. Moreover 'executive governance for the eurozone' may require some degree of external representation for the eurozone."

Eswar Prasad

Senior Fellow, Global Economy and Developmen; New Century Chair in International Trade and Economics

30

"Weak enforcement mechanisms."

Theodore Pelagidis

Nonresident Senior Fellow, Global Economy and Development

40

"Contrary to the national states where the sociological and national bonding is based on ethnicity and commonalities, the eurozone lacks such bonding materials apart from a common notion that we all belong to a Western civilization. The economic fabric could provide the basis for such a bonding to take place, however after the latest developments with the Euro crisis the inherent problems of this thinly united currency zone make it apparent that the political union is as of today a very distant vision."

Daniel Speckhard

Nonresident Senior Fellow, Foreign Policy, Center on the United States and Europe

40

"Institutions are very weak when it comes to accountability and robust governance. National level dynamics are still driving the discussions on eurozone crisis solutions. At the same time, European institutions continue to take a larger role in shaping the discussion and debate and are working to press the national players to make the necessary decisions to do just enough to keep the eurozone from collapsing and put changes in play for the medium term to strengthen resiliency."

Justin Vaisse

Director of Research, Center on the United States and Europe; Senior Fellow, Foreign Policy

40

"The eurozone needs stronger and more accountable institutions, and does not have them yet. It cannot just be an ever-stricter surveillance society, and needs citizen control, otherwise public opinion in creditor countries will feel cheated and public opinion in debtor countries will feel abused. A common budget and a Treasury, as suggested by Herman von Rompuy, would also help stabilize things, inspire confidence, and provide common projects benefitting all Euro member states. Delineation of powers with the EU may prove complex, however, and lead to a two-tier system."

75

"The EMU was voluntarily created as a single currency without a state; it is not surprising that facing a major and unexpected crisis existing mechanisms proved insufficient. The striking fact is that many new institutional and political mechanisms have been arranged at short notice and proved immediately sufficiently robust to resist the immense threats culminating in the end of 2011. Decisions have been repeatedly submitted to popular votes that have frequently shaken incumbent governments but constantly confirmed Euro-oriented successors; clearly imperfect in this phase of transformation, accountability of decisions has been constantly checked under the existing democratic rules with particularly eloquent examples in Germany with the repeated agreements of the Bundestag to costly/risky rescue operations and at the other extreme in Ireland where the Irish people adopted the fiscal treaty by a 2/3 majority in a referendum. A high level of resilience has thus already been proven; it will nonetheless take time to arrive at a fully developed political union; first down payment within 2 years, achievement, 10 years."

Andrew Moravcsik

Nonresident Senior Fellow, Foreign Policy, Center on the United States and Europe

90

"Political union, both in terms of vague executive power and especially in terms of democratic accountability, is a red herring. Most of the reforms that are necessary are national, not Brussels-based, and to the extent they are EU reforms, speaking vaguely about "political union" just clouds the issues. The issue of a "democratic deficit" is based on a fundamental misunderstanding about politics. Polling data shows clearly that in modern democracies, one policies are broadly "democratic," citizens do not favor, trust or like policies because they are more involved in their creation or because the institutions that generate them are more "participatory" (e.g. made by legislatures, referenda, or elected officials rather than courts, central banks, technocrats and executives). The question is whether the policy satisfies their preferences and the problem with the Euro is that currently it does not."

"In order to make the eurozone a viable currency union in the long term, European leaders need to make progress towards fiscal union, an objective that includes fiscal convergence among national budgets, a regime of centralized surveillance and enforcement of budget rules, It could include, as well, two even more controversial features: mutualization of debt and fiscal transfers in the form of a common budget. On a scale from 0 to 100%, how far along do you estimate the eurozone to be in achieving the desirable level of fiscal union?"

Carlo Bastasin

Visiting Fellow, Global Economy and Development, Center on the United States and Europe

20

"The formal framework is in place, but it responds only to the principle of strict surveillance. There is no sign of fiscal coordination. Even fiscal surveillance has proven disappointing in its first application when the European Semester 2011 fell short from being convincing and was even later revised by national member states. The recent attempts to build a "fiscal capcity" for the eurozone seem to wither away, while, significantly, negotiations on the EU budget have shown the first attempts to reduce the common pool of resources.

"

Eswar Prasad

Senior Fellow, Global Economy and Developmen; New Century Chair in International Trade and Economics

25

"Limited substantive progress."

Douglas Elliott

Fellow, Economic Studies, Initiative on Business and Public Policy

30

"In this area, permanent structures are fairly sparse and the EU/eurozone have had to make do with ad hoc arrangements that have been cobbled together to deal with the Euro Crisis. Europe can deploy very considerable financial resources through the ESM and, even more so, through the ECB. However, there are not good decision-making structures and political agreement to use these smoothly, effectively, and pre-emptively. Further, there is only a small common European budget to assist with imbalances and few common debt instruments, most of which are structured for the specifics of their task, such as for the EFSF.

"

Ernesto Talvi

Nonresident Senior Fellow, Global Economy and Development, Latin America Initiative

30

"Under the 'Fiscal Compact' 25 European economies have agreed on fiscal convergence and enforcement mechanisms, which are likely to become operative next year, once the treaty is ratified by at least twelve eurozone members.However, there is little advance in debt mutualization and common budget discussions. The content of the topics being discussed are well aligned with the objective of creating a stronger fiscal union, but significant political disagreements among eurozone members remain on these complex fiscal issues."

Donald Kohn

Senior Fellow, Economic Studies

35

"A road map for convergence and enforecement has been established but not yet tested and implemented. True mutualization of debt will require democratic reforms to be sustainable. Responsibility for repaying debt must be accompanied by democratic responsibility for how it is incurred. "

35

"Europe has made some strides toward this objective although what shape it will take is still highly controversial. If successful, the end product is more likely to be a compromise that a pure adoption of the US or other models that could still be good enough. But politics could still get in the way.

"

Daniel Speckhard

Nonresident Senior Fellow, Foreign Policy, Center on the United States and Europe

35

"While taking some dramatic steps this year in adopting new measures for surveillance and accountability on the budget side, including more oversight and potential penalties by the European Court of Justice, it remains to be seen how effective these will be in practice. There have been some indirect steps toward mutualization of debt, but still insufficient to truly protect the eurozone. Fiscal imbalances among countries remain large and are likely to be the case for some time giving the widely disparate economic, political and cultural situations among countries.

"

Domenico Lombardi

Senior Fellow, Global Economy and Development

40

"Progress has been achieved in terms of enhancing budgetary discipline through the Fiscal Compact treaty expected to come into effect shortly. But there is no credible roadmap wrt mutualization of debt and a central budget. The latter has now become even more important not only for the traditional purpose of enhancing cohesion and solidarity but also because lack of fiscal room deprives national economies of much-needed shock-absorber and insurance devices."